How your Credit Score affects your Mortgage Rate

Your credit score is the most influential determinant of your mortgage rate.

The higher your score, the lower your interest rate.

Not only is your credit score vital to get a low interest rate, it determines whether you can get a home loan at all. Typically, buyers with a credit score below 620 will struggle to secure a mortgage. It is still possible just much harder.

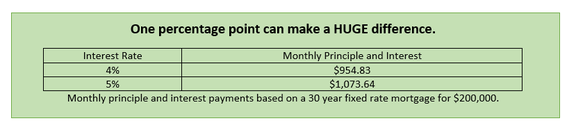

As you can see above, one point makes a huge difference.

A credit score of 740 or more should qualify for the best mortgage rates from most lenders. Depending on the lender, the mortgage rates offered to the highest and lowest credit tiers can vary as much as a full percentage point and a half.

Having good credit, could save you thousands on your mortgage.

What do lenders look for?

Lenders prefer borrowers with low balances, a long history of on-time payments and a mix of credit utilization -- for instance, a car loan and a couple of revolving accounts such as credit cards.

How do you clean up your credit?

Ideally you should check your credit score about a year before you plan to purchase your home, this way you have time to correct errors and improve your score.

Federal law entitles you to a free copy of your credit report once every 12 months from the three major credit-reporting agencies: Equifax, Experian and TransUnion.

Take the time to comb through your credit reports to be sure your name is spelled correctly, your address is correct, check to be sure each and every account is yours and reported accurately. If you have closed an account be sure that the information is accurate.

If you're buying a home soon, try not to apply for new credit. Sometimes you can't avoid it -- for instance, if you need a car loan or college financing. You should resist opening several new lines of credit in a short time. Multiple new accounts can decrease your credit score.